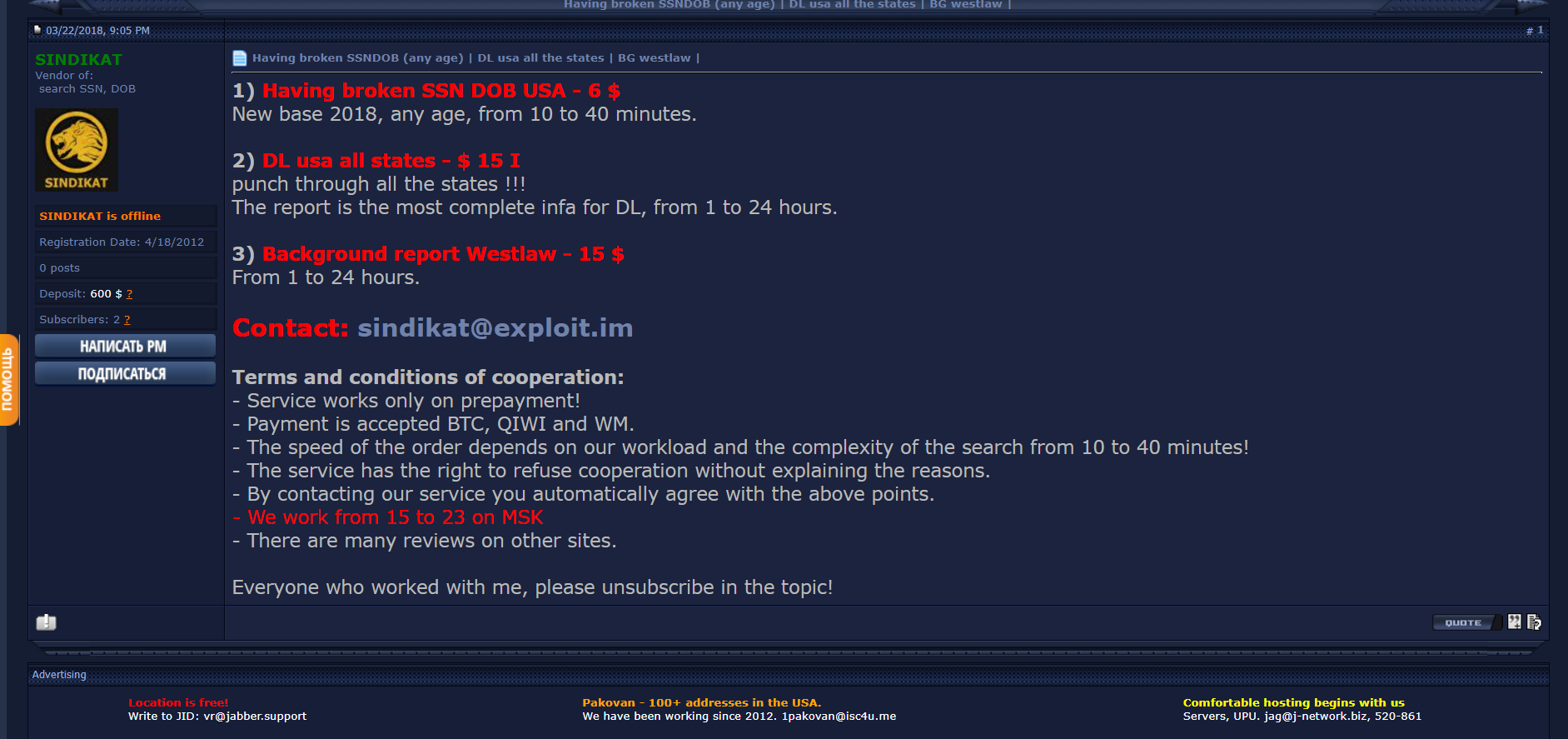

Synthetic Identity Theft: The $6 Billion Fraud Epidemic Hiding in Plain Sight

Synthetic identity theft exploits fundamental flaws in America's credit system. Our whitepaper reveals how fraudsters create fake personas from real SSN fragments—and what institutions can do to stop them.

Synthetic Identity Theft: The $6 Billion Fraud Epidemic Hiding in Plain Sight

Unlike traditional identity theft—where criminals steal an existing person's identity—synthetic identity theft involves creating entirely new personas by combining real data fragments with fictitious information. It's a fraud scheme that exploits the very mechanisms designed to give people access to credit.

The Mechanics: How Synthetic Identities Are Born

Synthetic identity fraud follows a predictable three-phase lifecycle:

Phase 1: Assembly

Fraudsters combine a real Social Security Number (often belonging to children, elderly individuals, or the deceased) with fabricated names, dates of birth, and addresses. The SSN provides the anchor of legitimacy; everything else is fiction.

Phase 2: Cultivation

The synthetic persona is "aged" through techniques like piggybacking as an authorized user on legitimate accounts or applying for secured credit products. Over months or years, the fake identity builds genuine-looking credit history.

Phase 3: Exploitation

Once the credit file is mature, fraudsters execute a "bust-out"—maxing out all available credit simultaneously and abandoning the identity. By the time lenders realize what happened, the perpetrators have vanished.

The Systemic Vulnerability

The U.S. identity system suffers from a fundamental design flaw: the Social Security Number functions as both a public identifier and a private authenticator. This dual-purpose role—what security experts call a "shared secret"—makes the entire system vulnerable.

Current verification methods often confirm that an SSN exists in records but fail to verify whether the applicant is the rightful holder of that SSN. This verification gap is precisely what synthetic fraudsters exploit.

The Scale of the Problem

The numbers are staggering:

- $6 billion in estimated lender losses (2016 industry estimate)

- 548+ million SSNs issued as of 2025—many belonging to deceased individuals or remaining unassigned

- 30-40% reduction in synthetic fraud achieved by institutions implementing eCBSV verification

Who Creates Synthetic Identities?

The actors range widely:

- Organized crime syndicates operating at industrial scale

- Individual fraudsters seeking quick profits

- "Survival-motivated" individuals—undocumented immigrants seeking financial access, domestic violence survivors escaping abusers, or others with legitimate reasons to avoid their legal identity

This diversity of actors complicates enforcement and highlights how systemic failures create opportunities for exploitation.

Recommendations for Defense

For Financial Institutions

- Implement eCBSV: The Social Security Administration's electronic Consent Based SSN Verification API verifies the binding between SSN, Name, and Date of Birth

- Layer defenses: Combine authoritative checks with behavioral analytics to identify cultivation patterns before bust-out occurs

For Policymakers

- Mandate eCBSV integration for all federally-regulated institutions

- Regulate data brokers to restrict practices enabling mass aggregation of identity fragments

For Consumers

- Use credit freezes proactively—especially for children's SSNs

- Minimize SSN disclosure to non-financial entities

Download the Full Whitepaper

Our comprehensive research paper provides deep analysis of synthetic identity theft mechanisms, regulatory gaps, and defensive strategies.

Mindwise Whitepaper: Synthetic Identity Theft

Synthetic identity fraud isn't just a financial crime—it's a symptom of an identity infrastructure built for speed rather than security. Understanding the mechanics is the first step toward building resilient defenses.

Contact Mindwise to learn how our intelligence platform helps financial institutions detect synthetic identity patterns before the bust-out occurs.